As we spend the days in full celebration ushering in the new year, your medical insurance company is resetting the clocks on your deductible. It is important for you to understand your medical benefits and policy details so that you can maximize your benefits and out-of-pocket expenses, as well as let you know exactly what you are responsible for. This can help you better plan the rest of the year and avoid unexpected medical bills.

There are plenty of theories about money and medical insurance management. We recommend that using high-ticket medical expenses, such as medical imaging, at the beginning of the year to get your deductible out of the way — especially if it is elective and will only be partially covered anyway. This allows you to rest assured knowing that the rest of the year, knowing you will be covered at the maximum rate for all other qualified medical expenses. Making a plan and scheduling appointments that help meet your deductible early on in the year allows you to plan out your expenses better and be prepared for unexpected or emergency events throughout the year.

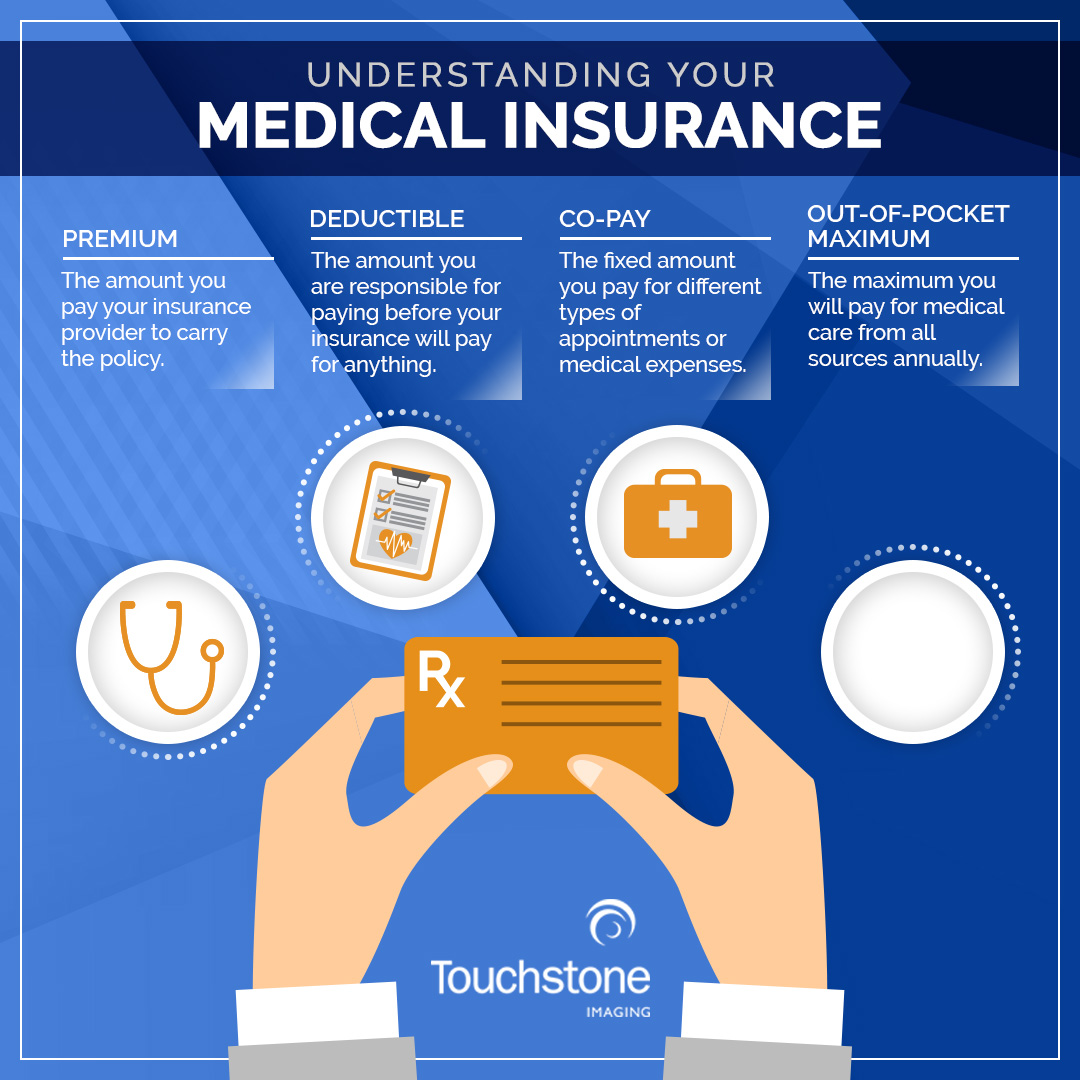

Understanding Your Medical Insurance

Let’s take a minute to discuss the basics of medical insurance and how it affects what you pay. There are a few terms that you should understand about your insurance:

Premium

An insurance premium is a monthly fee that you pay to have your medical insurance. Sometimes your provider pays a portion of this or you can pay a third-party insurance provider the premium. Whether you pay each month, quarterly, twice a year, or annually, the premium is the amount you pay simply to have the insurance policy. Your premium will vary based on the provider, the options you select, and what your plan covers. Generally speaking, the more your plan covers, the higher your premium might be. Some people attempt to lower their premium by opting to pay higher deductibles and co-pays. The good news is, your premium should be taken out of your paycheck pre-tax and medical expenses are tax-deductible.

Deductible

Your deductible is the annual amount that you are responsible for paying for your healthcare expenses each year before your insurance will pay the maximum amount. Your deductible is determined by your policy and can range from as low as $200 for a high-premium policy to nearly $10,000 for a very low-premium policy. You can often choose your deductible and most people base it on their health status and normal medical expenses. For instance, if your insurance has a $1,000 deductible, you will have to pay all medical expenses before your insurance will begin to pay anything, regardless of your copay.

This is what we were referring to at the beginning of our post. If you know that you have medical expenses, such as an MRI, it is wise to schedule those at the beginning of the year when you can plan and budget for them. Once you have met your annual deductible, your medical insurance should cover you for the rest of the year. This is particularly helpful in the event of unplanned or emergency medical events. Plan for it on your terms rather than being caught off guard.

Co-Pay

A co-pay is a set price that you pay for certain medical services, as defined by your plan. While most plans cover preventative screenings and checkups at 100%, routine doctor visits, emergency room visits, procedures, and prescriptions may incur a co-pay. It is typical to have a reduced co-pay for your primary care provider and a slightly higher co-pay for specialists. For instance, a co-pay for a primary care provider may be $25, whereas, a visit to your cardiologist may cost $40.

It is important to note that until your annual deductible is met, you will pay 100% of your medical visit’s cost. Once your deductible is met, you will only be responsible for your co-pay.

Out-of-Pocket Maximum

The out-of-pocket maximum is an amount set by your policy that places a cap on your out-of-pocket expenses in a year from all sources. This includes co-pays, deductibles, and any co-insurance. Out-of-pocket maximums are determined in your policy, but cannot exceed the federal limit of $8,150 for an individual or $16,300 for a family. For general appointments and routine medical visits, you likely won’t have to worry about your out-of-pocket maximum. However, in emergency situations or chronic medical conditions, between deductibles and co-pays, the expenses can stack up. For instance, if your medical insurance policy has an out-of-pocket annual expense of $3,500, once you pay $3,500 from all sources, your healthcare insurance will pay 100% of the remainder of your medical services.

Understanding your medical insurance policy involves much more than selecting an in-network provider and facility. Once you understand the basics of your insurance coverage, you can better plan for the financial aspects of your medical care. It is a wise idea to contact your insurance provider before any procedure to ensure that it is covered. If it is not, scheduling those appointments at the beginning of the year will help you maximize what is covered.

At Touchstone Imaging Centers, our goal is to provide quality medical imaging services at an affordable price. We understand that diagnostic imaging services can be expensive, but we also know the value it can provide to your care and outcome. We take most major insurances, including Medicare and CareCredit. We offer financial assistance for qualifying patients and will work with you to make paying your bill as stress-free as possible. Contact us to find out more about your costs and schedule your appointment today!